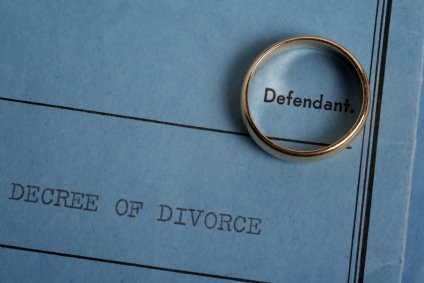

Yes, your spouse is the one who used the credit cards. Yes, your spouse got the house in the divorce. Yes, you each kept your own cars and you’ve both been making the payments.

His / her finances have nothing to do with you and haven’t for a long time. Right?

Wrong. Not unless your divorce included closing all your joint accounts and opening new ones in your individual names. Just because your divorce decree said that one spouse was responsible for this debt and the other spouse responsible for that one, as far as your creditors are concerned you’re both responsible.

Why? Because they can. If you both signed the application forms for credit cards, you’re both on the contract and you’re both liable.

Therefore, if your spouse has suddenly stopped making those payments, the black mark will show up on your credit report, and the creditors will come looking for you to make the payments.

To be removed from a joint account, you need to cancel the account. Not a good thing for your credit scores, but necessary if you really want to sever that tie. I suggest doing it immediately after a divorce rather than waiting until there’s a problem. Remember, you’re liable for all charges on the account as long as you remain a joint account holder.

You say you didn’t sign the application – your spouse had that credit card when you married and you were just added as an authorized user after the marriage. In that case, you won’t be liable for the debt, but the default will still show up on your credit card.

For several years FICO stopped factoring authorized user status into credit scores. Since becoming an authorized user on an account was helping people raise their scores, some crafty entrepreneurs began selling such use. When FICO realized what was happening, they put a halt to it.

But now they believe they’ve figured out how to filter out any bogus users and they once again factor it in. That’s wonderful if you’re a youth trying to piggyback your parent’s good credit to build your own – not so wonderful if your X-spouse is not paying his or her bills.

The owner of the account can contact the credit card issuer and ask to have an X-spouse removed as an authorized user. If he or she refuses, you can file a “not mine” dispute with the credit bureaus. Remember that it will take them at least 30 days to act, so if you need to do this, get started.

Then there’s your home mortgage. As with credit cards, the mortgage holder is not going to let you off the hook just because it was awarded to your spouse in the divorce decree and you haven’t lived there for 6 years. They won’t even care if you’re not on title – as long as you’re on the contract.

Some believe that signing a quit claim deed to the spouse absolves them of responsibility – but it just isn’t so. If your spouse lets that house go into foreclosure, your credit score will be equally harmed.

If you’re divorced, play it safe. Order your free credit report today and find out if your X-spouse’s activities are still being reported on your credit file. Do it now, before you need credit and find that “you” are not a good credit risk.

Stereotyping is not nice. We all know that, but there’s a reason why a “slick dealer” is often referred to as a “used car salesman.”

Part of that reason has to do with misrepresenting cars, but another part of it has to do with financing. They have enough ways to juggle the price of the car, the price of your trade-in, and the associated fees to keep anyone’s head spinning.

Of course, they’ll say all their number jugging is in your best interests – perhaps to make it appear that you have a larger down payment – or that you even have a down payment. Often, they’ll tell you the car you’re trading in isn’t worth any more than you owe, but they can pretend it is…

So pre-arm yourself before you step foot on a car lot. The first thing you should do is order a copy of your credit report and look at the scores. If you don’t know your own scores, the dealership can tell you anything – and some of them will. Then they’ll quote you a higher interest rate based on your “low credit scores.”

If your scores really are low and you can see some ways to bring them up – do it before you go shopping.

Next, don’t let anyone check your credit report until you’re actually ready to buy. Checking 2 or 3 lots over the course of a few days will only count as one inquiry, but if you shop now and then wait 6 weeks to buy, your earlier shopping will have harmed your credit score.

Now for the questions you must ask:

• What is the actual cost of the vehicle?

• How much am I financing after I pay $X down?

• What is the true APR on that financing?

• What is the total number of payments?

• What is the exact amount of each payment?

• And that adds up to … how many dollars in finance charges?

• Are there any fees you haven’t yet disclosed?

• Are you requiring credit insurance? If so, what does it cost?

• When I drive off your lot, is this purchase finalized?

That last question seems odd, but it’s an important one, because it can catch you unawares.

Many car dealers engage in a version of “bait and switch.” They send a new owner home with a car and a loan. Then in a day or two they call and say they’re terribly sorry, but the lender refused to make the loan. …But don’t worry, they’ve found someone else who will. Of course, the rate and the payment are a bit higher, but…

Don’t go for this. Unless you see documents that spell out every one of the terms of your loan, and unless you feel confident in an assurance that this is the FINAL deal, don’t take the car off the lot. Make sure you know who the lender is, and that you see their approval – in writing.

This “bait and switch” tactic is known as the “puppy dog close.” The dealer knew that you wouldn’t agree to pay a high interest rate right off the bat, so he didn’t even try. Instead he sent the “puppy” home with you for a couple of days – just long enough that you wouldn’t want to part with it and would go along with the rate and terms he intended to give you in the first place.

If you are in need of a auto insurance quote, check out……autoinsureanceqoutefast.com

Do you remember life before mortgage brokers? If you needed a loan, you went to “your” bank and sat down with the loan officer. Often, you had to have an account with that bank or they wouldn’t even talk to you.

After you explained your needs the bank would decide whether or not you could buy that house, or car, or get the money you needed for some other purpose. If they turned you down you could go talk to some other bank and hope for a different answer. If they said yes, then you took the loan program they offered or didn’t get a loan.

Then came mortgage brokers. They had access to loans from a wide variety of banks, and those banks had different programs for different kinds of borrowers. Some, such as the sub-prime loans, were ill-advised, but the banks offered them and your local mortgage broker could help you get in.

Now the trend is reversing, and many mortgage brokers believe they will soon be out of business.

JPMorgan Chase and Citi recently announced they will no longer accept loan applications submitted through brokers. If you want to do business with them, you have to go sit down with one of the bank’s loan officers. If there are none near you, you can make application over the phone or on line.

One reason banks say they are making this move is to “better serve the consumer” by putting them in the right loans. They’re trying to blame brokers for the loan programs the banks themselves promoted and the “bad loans” that their underwriters approved.

Some banks, such as Wells Fargo, still believe in working with brokers, but they may be a dying breed.

This trend is, of course, a loss for consumers. Brokers were able to “shop their loan” among a variety of banks and find the program best suited to the individual consumer. If necessary, they could switch the loan from one bank to another, saving the consumer from re-submitting loan applications at a variety of banks.

They are also more accessible to consumers. Banks close on time and are rarely open on week-ends. Mortgage brokers make themselves available to their customers during week-end and evening hours.

Mortgage brokers are also more responsive to providing the hand-holding that some consumers need. Activities such as alleviating fears, helping find lost documents, and explaining procedures are all part of a days work for a mortgage broker. It isn’t likely that bank loan officers will offer the same kind of personal service.

Along with a loss in service, some in the industry believe that the elimination of mortgage brokers is a first step in the direction of higher loan fees due to lack of competition. Most working consumers simply don’t have the time to visit every bank – either in person or on line – to make application, compare rates and fees, and make a decision.

This is a great question. Where did all the money go that was being pumped into our economy from 2002 to 2006? It seems like all the money globally disappeared overnight. The truth to the matter is there was never any money. Everything that was being bought and sold was on credit.

The banks, credit card companies, car dealerships, and other creditors were extending credit to everyone. These creditors also were lowering there credit standards. There is a reason why the current credit scoring process is in place. The FICO score model is calculated risk software that determines the likelihood of a borrower paying back a creditor. Evidently the creditors were ignoring this risk based software.

I am sure you can remember all the 0% interest rate loans on furniture, electronics, cars etc……… Some of these advertisers also sold you that there would be no payments for 3 years. This type of activity made no financial since, since people with high risk scenarios were being granted loans they could not afford.

With lending “its back to the basics”, if you cannot afford the loan, you don’t buy. I strongly disagree with getting furniture and electronics on 0% interest cards. My thoughts on this are what if you loose your job. How are you going to pay all of this off?

Now you are stuck with 0% interest loans that you cannot pay back.

This is what happened during the last 2 years. All of these loans started failing because of a recession and families over extending themselves. Is a Depression lurking around the corner? Unemployment during the “Great Depression was up to 25%. Now don’t get too alarmed yet, currently the unemployment rate is 8.5%. This unemployment rate is expected to go up to 10% by the end of the year.

There are signs of improvement in the market because of companies trimming the fat. Current economists claim we have hit rock bottom and are seeing signs of a recovery.

Needless to say, we as Americans are going to find ourselves in a different lending market. The requirements are going to be stringent. We are going to be required to have better credit scores and more savings to get loans.

Bottom line; don’t buy stuff on credit that you cannot afford to pay back the next month. If hard times fall in your lap, you might find a collection company calling you at work, at home and even on your cell phone.

Lets be smart for now on, and only purchase stuff we need…..

If you’re having trouble meeting mortgage payments, you certainly are not alone.

The Mortgage Bankers Association recently reported that the national foreclosure rate is now at 3.3%, and over 11% of all mortgages are either delinquent or in the process of foreclosure.

Now, due to the state of the economy, even some homeowners who are still managing to keep up with payments are being tempted to abandon the mortgage and start over.

If you’ve been thinking of making that move, first consider what it will do to your credit rating.

A repossession on your credit report will instantly reduce your FICO score by at least 100 points – and it doesn’t matter if you walked away voluntarily or were forced out through foreclosure.

Worse, after a foreclosure, the lender can still come after you for any difference between what you owed and what they are able to gain through the eventual sale of the house.

For some, a better alternative is the short sale. In this case, the bank agrees to forgive that difference and mark your debt paid. If you’re very lucky, they will even report it to the credit bureau as “paid satisfactorily” so that it doesn’t damage your credit score. If they report it as “settled for less than the full amount due” your score will take a hit, just as if you’d gone through foreclosure.

The big benefit is that if this was your primary home and the forgiven debt was less than $1 million ($2 million for couples filing jointly) then you will not owe income tax on the forgiven debt. This, by the way, is a temporary tax law change and only affects debt incurred between 2007 and 2012.

A better alternative to either foreclosure or a short sale is negotiation. Lenders really don’t want to own houses. It costs money, and what they want is money coming in, not going out.

If you’re falling behind financially, contact your lender right away and work to negotiate a lower rate or other terms that will allow you to keep the house and stay afloat.

If you need help with these negotiations, you can get it – at no charge. The National Foundation for Credit Counseling recently got $16 million in federal funding to help troubled homeowners, and has trained counselors who will assist in negotiations.

HUD also has approved counselors in every state who don’t charge anything to help homeowners stay in their homes. To find a counselor in your state, go to http://www.hud.gov/foreclosure/local.cfm

Under the Homeowner Affordability and Stability Plan, the government is offering help to up to 9 million families so they can avoid foreclosure. So don’t wait – if you need help, ask for it.

Note* The National Foundation for Credit Counseling warns that it is not necessary to pay for help with your negotiations. Stay away from companies that offer to help for $500, $1,000, and even $1,500. Often these services are bogus – and they’re always available for free.

That depends upon the policies the card issuer has. American Express, for example, says they report new credit card accounts one billing cycle after the application was approved – regardless of whether the card was activated.

Your application for the card will always show up – and will remain for 2 years. However, it will only be factored into your credit score for one year.

Once a credit card account has been approved and reported to FICO, it will show on your credit report as an active account until it is closed. Your non-use of the card is only considered as a part of your overall debt to available credit ratio.

Credit card Adviser Leslie McFadden at Bankrate.com advises that canceling a card after the issuer reports it could negatively affect your credit score. If you cancel before it is reported, it will have no affect.

Thus, if you made application for one card but received another – and you don’t want the card you were issued, you should cancel immediately. This is not unusual in today’s credit climate. Credit card issuers hoping to attract card holders with high FICO scores advertise low rates and high credit lines, but often issue cards bearing high rates and low credit lines after reviewing an application.

While this will upset you – it shouldn’t make you feel less worthy. Almost everyone is seeing their FICO scores decline due to the actions that card issuers are taking today.

Shrinking credit lines means card holders who once had a 30% debt to available credit ratio now have an 80 or 90% ratio. Closing unused accounts has the same effect. Card issuers are doing both, and it is affecting people who once had enviable FICO scores.

Should you receive a card in the mail that you know you didn’t ask for, and that isn’t merely a replacement of a card you carry that is expiring, you should contact the issuer immediately to cancel it.

You probably won’t be able to get much information over the phone about who initiated the request – or when or where. So your next step should be to order a copy of your credit report. That unsolicited card could be a sign of identity theft, so look for any other suspicious activity, especially signs that you have a new address or have made application for other credit.

I have heard so many negative stories and myths about Mortgage Brokers. This bad stigma that has been spread about brokers is very intriguing. Typically when you talk to a seasoned Realtors they will say just the opposite. Normally what you will hear from a Realtor is use a mortgage broker. I wanted to discuss some of the differences between a bank and a mortgage broker in this article. Banks

You will find that most banks providing mortgage loans work with only good credit. This has been the case for years. Also with banks there is more red tape to get a loan done than with a mortgage broker. This is why most Realtors use a broker. Mortgage brokers have the ability the package loans better. In other words they know how to get the loan done so the loan can be sold on what is called the secondary market. Some banks don’t sell their loans, so they are extremely picky with how they underwrite loans that they portfolio. Don’t get me wrong, banks sell their loans on the secondary market also. Bottom line, banks are just pickier on their underwriting criteria. One advantage of banks is their underwriting fees are typically less, but not by much. This difference usually ranges between $300 to $500 dollars in cost to you. In some cases the banks fees are higher than brokers. This cost usually means the difference of getting approved or denied. So my question would be, is it worth the extra cost to have the loan go smoothly? I would have to say yes. Another disadvantage of Banks is if your loan runs into problems because the underwriter does not like something, you are stuck. A bank cannot broker the loan somewhere else to get a second opinion if they run into issues. This is the single biggest issue with Banks.

Brokers

I have found that most broker shops have the tendency to be more knowledgeable about loans. I believe the reason is Mortgage Broker’s are more motivated to get loans done properly because they make good money per loan. Money motivates anyone. Loan officers with banks make less on their loans, so I believe this promotes high turnover along with a lack of proper training. Also if a broker runs into issues typically they can repackage the loan and send it to another participating wholesale lender. These lenders range from big banks to small banks. In the world of underwriting every underwriter might view a file differently. This is the HUGE advantage of using a broker. There is no bigger disappointment than being told no on your dream house. So I recommend that you use a reputable mortgage broker in your area. Don’t get me wrong, there are some real bad mortgage brokers out there. So make sure you are working with a seasoned mortgage broker.

In regards to the differences in process, there really is not much difference. The underwriting guidelines for FHA and Conventional loans are pretty standard across the board for banks and Brokers. The main difference is flexibility to fix issues. As mentioned you can see that a Mortgage Broker might have more flexibility to get loans done and shop for better interest rates on your behalf.

With the mortgage credit score benchmark changing monthly, it’s really tough to keep up with what the requirements actually are. As the market changes like Texas weather, you can only assume you have a high enough credit score to even get a mortgage loan. This market has been extremely turbulent with all the new mortgage qualifying guideline. I wanted to give the current credit score requirements as of March 29, 2009 for FHA and Conventional loans.

FHA credit score Requirements- Most lenders are requiring that you have a 620 credit score to get a FHA mortgage loan. This benchmark has recently changed from a middle credit score of 580 to a 620 with most lenders. There might be circumstances out there where a lender will allow a loan below this benchmark if they don’t plan on selling there loans on the secondary market. I do know that you will find most lenders will require a 620 score to get you financed. I know this rule will be applied to all brokers, and not to all banks. So you might check around just to see if there is a bank allowing a credit score below 620 and what there guidelines are. Historically brokers have always been able to get loans done that banks cannot do. It looks like the tide might be changing a bit in this arena.

Conventional Loan credit score Requirements – Currently with most lenders you have to put down between 5 and 10%. You must also have a minimum of a 700 middle credit score to get financed. This is largely due to (Mortgage Insurance) M.I. companies clamping down on credit criteria to insure a loan. However there are some banks that get special privileges that other don’t. For example, some banks can now get you a Conventional loan with a credit score as low as 680 with 10% down. These M.I. companies have chosen to allow this with certain qualified banks. You will find that most lenders will require a minimum 700 credit score to get financed, and don’t forget you must qualify as well.

VA and USDA credit score requirements – These two loans are really the only loans left that are 100% financing still. They both are government insured loans and you must qualify for each program. Not everyone will qualify for either one of these government loans. The current market for these particular loans does require a middle credit score of 620. USDA has had this credit score requirement for quite some time now. So this is nothing new with this particular loan.

What is going on in our country? We don’t want to offend anyone, or say anything that might hurt someone’s feelings. Wow, so I guess if you are wrong that is ok. I BEG to DIFFER. I think we need to spread the word that if you are wrong, then you are WRONG. I am not really concerned what everyone else thinks, the only person that really matters is what GOD thinks, not some politically correct person.

Let’s face the facts, when you are wrong about something it needs to be known. Whether it’s in regards to finance, political views, religion or just shop talk. There are right ways and wrong ways to doing things.

I wanted to take my real approach to views about what is really going on. I would like to call it the Back to Basics show. If you ever have a chance, listen to Mark Levin. This guy takes the correct approach to saving our Constitution, and telling the FACTS about what is really going on in our country.

Whether your credit stinks, or your political views are radical, I will tell you what is right.

Since my site is mainly about credit and finance, I will stick with the general content and topic of this article. If you currently are not RICH, your credit is more important than ever. I cannot imagine what your life will be like if you need a loan and cannot get one. With the lending institutions increasing credit score requirements and qualifications rules, you can count on your life being extremely tough with challenged credit. So the question is what do you do about it? Within my site I have all kinds of articles about what you need to do to manage your credit, or fix it. I get e-mails daily from people all around the U.S. thanking me for writing about the FACTS. You can go the http://www.ftc.gov/bcp/edu/pubs/consumer/credit/cre13.shtm and see that SELF Help credit repair is the recommendation by your own government. This should tell you something. There is no quick fix to getting your credit report cleaned up. Don’t fall prey to quick fix credit repair schemes. Use our site to help yourself out. I should know since I am a lender and help people out all the time that will listen. Search within our blog and find the article that fits your circumstances.

For once I am not going to be politically correct within my blog. So the point is, “If your credit stinks do something about it.” Don’t depend on some credit repair scam. This information provided today is for your own good. I don’t make any money by educating someone on how to repair their own credit report. I thought I would mention this. There are rules and steps you need to take in order to clean your mess up. Once these steps are understood teach them to your children. Help them; teach them to be responsible for their tomorrow.

In this country we have many freedoms. One of our freedoms is the pursuit of happiness. Now, how we get to this happiness is by what we feel is right and we seem to not follow good advice if the advice requires some effort. Repairing your credit requires effort on your part.

If I had a dollar for every time I have heard this from some potential home buyer I would be a millionaire. I am not sure where this ignorance comes from, but just because you think you have the credit to buy a home does not mean you will “QUALIFY.” It does not matter what anyone thinks, I do know that there is a proper process to buying a house. I wanted to educate the common public on how important it is to listen to a real estate professional that has a good reputation. I know you have probably heard about all the nightmares about how someone had a horrible experience while buying there home. This typically is the result of the wrong process. Here are the FACTS.

Get approved to buy- The first step before you look at homes, drive around, search the web, etc….. is to get with a lender and get pre-approved. It does not matter what you think or how you feel this is your FIRST step. If you don’t do this first and you fall prey to a realtor willing to drive you around to look at homes, you will have problems. The rules for lending have currently changed. Obviously with the new lending guidelines it makes only rational sense to see what you can qualify for, before you have a Realtor show you a bunch of homes you may not be able to buy. I never have understood why Realtors run buyers out to show them homes without getting them pre-approved first. Usually when a realtor does this, it is lack of experience and bad judgment on there part. So, before you look at homes, get pre-approved. This means have a lender run your credit report, and verify ALL documentation supporting what you have told that lender. If a lender does not ask for documentation supporting your income, and funds to close, that lender is not following the proper process to get someone pre-approved. A lender should not pre-qualify you, but pre-approve you. There is a difference. Getting pre-approved means the lender has verified what you have told them. Pre-qualified means the lender has pulled your credit report, but has not verified your documentation. This is where lots of issues will arise. Again, “Get Pre Approved…..

Get with a reputable Realtor- Once you have got pre-approved get with a seasoned real estate agent. Real Estate agents that are seasoned will know how to make your buying process smooth. A good Realtor will know your local market and how to find exactly what you are approved to buy. One of the biggest misconceptions out there is “I don’t want to pay real estate fees. Well guess what? You will pay them regardless, because all homes for sale are listed with a agent. Yes, there are some for sale by owners, and 99% of the time those homes are overpriced, because the owner is not educated enough to know his or her own market. So with this being said, you will need a Realtor to represent you.

I hope this article did not sound like I was shouting. I just see so many people not listening. I can only lead a horse to water, but I cannot make him drink.

Disclaimer: This information has been compiled and provided by CreditScoreQuick.com as an informational service to the public. While our goal is to provide information that will help consumers to manage their credit and debt, this information should not be considered legal advice. Such advice must be specific to the various circumstances of each person's situation, and the general information provided on these pages should not be used as a substitute for the advice of competent legal counsel.

Yes, your spouse is the one who used the credit cards. Yes, your spouse got the house in the divorce. Yes, you each kept your own cars and you’ve both been making the payments.

Yes, your spouse is the one who used the credit cards. Yes, your spouse got the house in the divorce. Yes, you each kept your own cars and you’ve both been making the payments.